Via Capitale Blog Articles on home financing, home decor & renovations

- Hidden Costs When Buying a Home

Buying a home is one of the most important financial decisions in life. However, many buyers focus only on the purchase price and overlook the hidden costs of buying a property.

- Here are the 7 most common mistakes to avoid when selling your home.

Many sellers make costly mistakes that can reduce their selling price or delay the transaction.

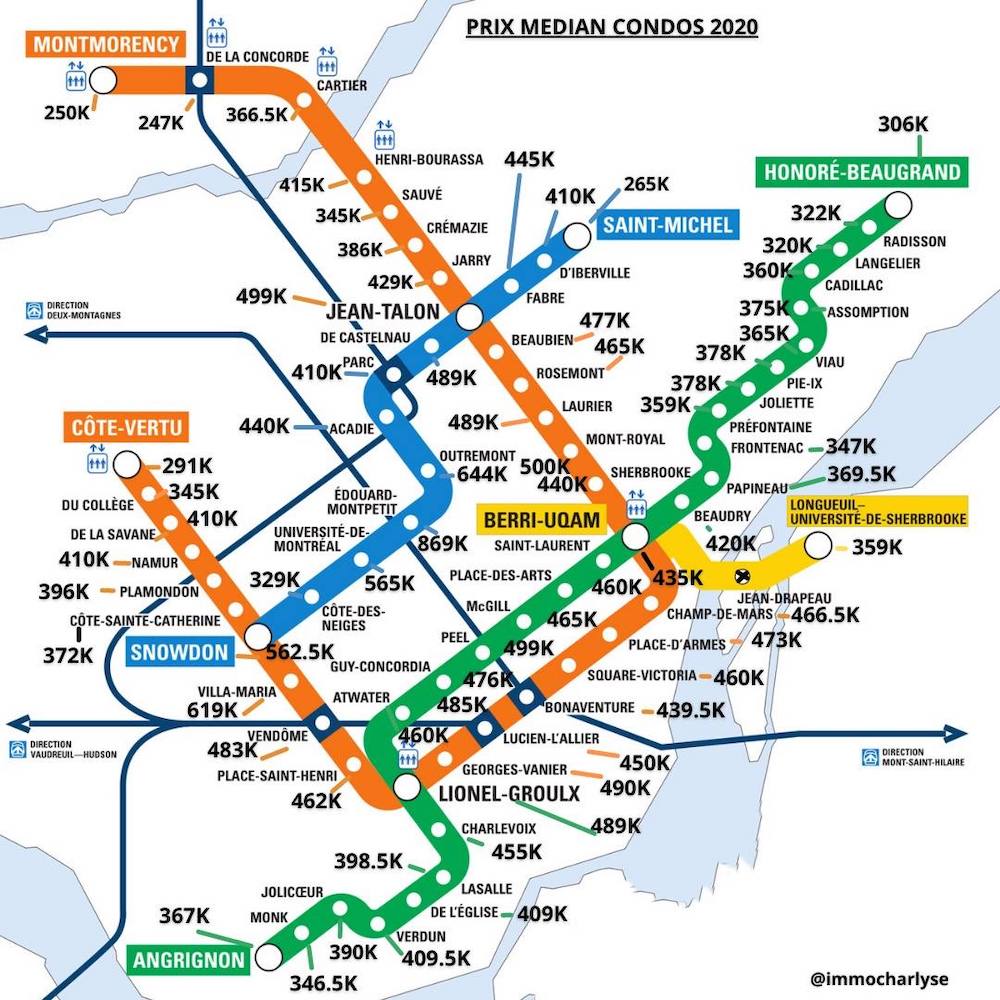

- The Quebec Cities Where Home Prices Are Rising the Most in 2026

Quebec’s real estate market continues to evolve in 2026, and some cities are clearly standing out with significant increases in home prices.

- Buying Before the School Year Starts: Why June Is Strategic with Via Capitale

Every year, the real estate market picks up speed as summer approaches. For many buyers, June is one of the best times to buy a home before the school year begins — especially with the support of Via Capitale real estate brokers.

- Spring: The Best Time to Buy or Sell in Quebec

As winter comes to an end, the real estate market begins to come back to life across Quebec. Spring is often seen as a strategic season for both buyers and sellers.

- 8 Essential Steps for Making Your First Real Estate Purchase a Success

Buying your first home is an exciting and essential step, and with our tips, you'll be ready to take the plunge with confidence.

- Summer Terrace: Ideas and Tips for The Perfect Space

Summer is the perfect season to get the most out of your terrace. Whether you like to relax in the sun or host cozy evenings, check out our ideas and tips to transform your outdoor space into a true summer paradise.

- Enjoy Summer: Invest in a Second Home

Find out why summer is the perfect time to invest in a second home, which is both a great getaway spot and a wise investment.

- Tips and Tricks for A Successful Move

Discover essential tips and tricks for a successful and stress-free move, from planning to unpacking.

- What to Look for in a Home Security System?

With so many options available, finding the right home security system can take time. Here are some tips to guide your research.

Selection:

- All

- 25th anniversary

- Achat

- Architecture

- Broker

- Collaboration

- Contest

- Courtiers

- Current Affairs

- Design

- EcoBroker

- Ecological

- Events

- Finances

- General

- Histoires de Montréal

- Histoires de Montréal

- Immobilier

- Lifestyle

- Moving

- Neighourhood

- Newcomers

- News

- Non Resident

- Property

- Propriété

- Purchase

- Quartiers

- Radio Series

- Real Estate

- Recommandations

- Recommendations

- Renovations

- Resale

- Rules

- Suggestions

- Suppliers

- Uncategorized

- Videos